Revenue-Meaning,Understanding,Examples,Types,Accrued and Deferred revenue (Commerce Achiever)

Revenue is the income generated from normal business operations and includes discounts and deductions for returned merchandise. It is the top line or gross income figure from which costs are subtracted to determine net income.

Revenue is the income generated from normal business operations and includes discounts and deductions for returned merchandise. It is the top line or gross income figure from which costs are subtracted to determine net income.

KEY POINTS

- Revenue, often referred to as sales, is the income received from normal business operations and other business activities.

- Operating income is income derived from normal business operations, such as sales of goods or services.

- Non-operating income is infrequent or nonrecurring income derived from secondary sources (e.g., lawsuit proceeds).

Understanding Revenue

Revenue is money brought into a company by its business activities. Revenue is also known as sales, as in the price-to-sales-ratio an alternative to the price-to-earnings-ratio that uses revenue in the denominator.

There are different ways to calculate revenue, depending on the accounting method employed. Accrual accounting will include sales made on credit as revenue for goods or services delivered to the customer. It is necessary to check the cash flow statement to assess how efficiently a company collects money owed. Cash accounting, on the other hand, will only count sales as revenue when payment is received. Cash paid to a company is known as a “receipt”. It is possible to have receipts without revenue. For example, if the customer paid in advance for a service not yet rendered or undelivered goods, this activity leads to a receipt but not revenue.

Types of Revenue

A company’s revenue may be subdivided according to the divisions that generate it. For example, a recreational vehicles department might have a financing division, which could be a separate source of revenue. Revenue can also be divided into operating revenue – sales from a company’s core business – and non-operating revenue which is derived from secondary sources. As these non-operating revenue sources are often unpredictable or nonrecurring, they can be referred to as one-time events or gains. For example, proceeds from the sale of an asset, a windfall from investments, or money awarded through litigation are non-operating revenue.

Examples of Revenue

In the case of government, revenue is the money received from taxation, fees, fines, inter-governmental grants or transfers, securities sales, mineral or resource rights, as well as any sales made.

For non-profits, revenues are its gross receipts. Its components include donations from individuals, foundations, and companies; grants from government entities; investments; fundraising activities; and membership fees.

In terms of real estate investments, revenue refers to the income generated by a property, such as rent, parking fees, on-site laundry costs, etc. When the operating expenses incurred in running the property are subtracted from property income, the resulting value is net operating income.

Are revenue and cash flows the same thing?

No. Revenue is the money a company earns from the sale of its products and services. Cash flow is the net amount of cash being transferred into and out of a company. Revenue provides a measure of the effectiveness of a company’s sales and marketing, whereas cash flow is more of a liquidity indicator. Both revenue and cash flow should be analyzed together for a comprehensive review of a company’s financial health.

How does one generate revenue?

For many companies, revenues are generated from the sales of products or services. For this reason, revenue is sometimes known as gross sales.

Revenue can also be earned via other sources. Inventors or entertainers may receive revenue from licensing, patents, or royalties. Real estate investors might earn revenue from rental income. Revenue for federal and local governments would likely be in the form of tax receipts from property or income taxes. Governments might also earn revenue from the sale of an asset or interest income from a bond. Charities and non-profit organizations usually receive income from donations and grants. Universities could earn revenue from charging tuition but also from investment gains on their endowment fund.

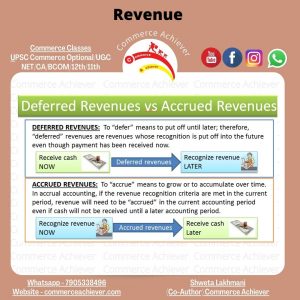

What is accrued and deferred revenue?

Accrued revenue is the revenue earned by a company for the delivery of goods or services that have yet to be paid by the customer. In accrual accounting, revenue is reported at the time a sales transaction takes place and may not necessarily represent cash in hand. Deferred, or unearned revenue can be thought of as the opposite of accrued revenue, in that unearned revenue accounts for money prepaid by a customer for goods or services that have yet to be delivered. If a company has received prepayment for its goods, it would recognize the revenue as unearned, but would not recognize the revenue on its income statement until the period for which the goods or services were delivered.

Can a company have positive revenue but negative profit?

Yes. A company has a cost to produce goods sold, as well as other fixed costs and obligations like taxes and interest payments due on loans. As a result, if total costs exceed revenues, a company will have a negative profit even though it may be bringing in a lot of money from sales.

You may also like