Book keeping(Objectives of accounting) (Commerce Achiever)

Bookkeeping is the recording of financial transactions, and is part of the process of accounting in business and other organisations. It involves preparing source documents for all transactions, operations, and other events of a business. Transactions include purchases, sales, receipts and payments by an individual person or an organization/corporation. There are several standard methods of bookkeeping, including the single-entry and double-entry, bookkeeping systems. While these may be viewed as “real” bookkeeping, any process for recording financial transactions is a bookkeeping process.

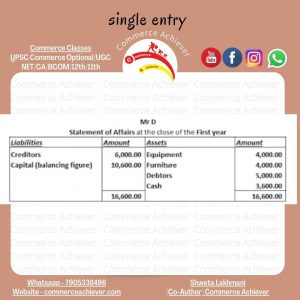

Single-entry system

The primary bookkeeping record in single-entry bookkeeping is the cash book, which is similar to a checking account register , except all entries are allocated among several categories of income and expense accounts. Separate account records are maintained for petty cash, accounts payable and receivable, and other relevant transactions such as inventory and travel expenses. To save time and avoid the errors of manual calculations, single-entry bookkeeping can be done today with do-it-yourself bookkeeping software.

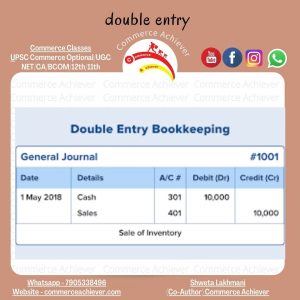

Double-entry system

A double-entry bookkeeping system is a set of rules for recording financial information in a financial accounting system in which every transaction or event changes at least two different nominal ledger accounts.

Double-entry bookkeeping, in accounting, is a system of book keeping where every entry to an account requires a corresponding and opposite entry to a different account. The double-entry has two equal and corresponding sides known as debit and credit. The left-hand side is debit and right-hand side is credit.

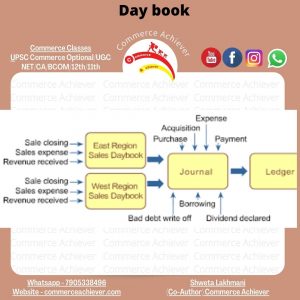

Day books

A daybook is a descriptive and chronological (diary-like) record of day-to-day financial transactions; it is also called a book of original entry. The daybook’s details must be transcribed formally into journals to enable posting to ledgers.

Daybooks include:

- Sales daybook, for recording sales invoices.

- Sales credits daybook, for recording sales credit notes.

- Purchases daybook, for recording purchase invoices.

- Purchases debits daybook, for recording purchase debit notes.

- Cash daybook, usually known as the cash book, for recording all monies received and all monies paid out. It may be split into two daybooks: a receipts daybook documenting every money-amount received, and a payments day book recording every payment made.

- General Journal day book, for recording journal entries.

Petty cash book

A petty cash book is a record of small-value purchases before they are later transferred to the ledger and final accounts; it is maintained by a petty or junior cashier. This type of cash book usually uses the imprest system: a certain amount of money is provided to the petty cashier by the senior cashier. This money is to cater for minor expenditures (hospitality, minor stationery, casual postage, and so on) and is reimbursed periodically on satisfactory explanation of how it was spent. And also the balance of petty cash book is Assets.

Journals

Journals are recorded in the general journal daybook. A journal is a formal and chronological record of financial transactions before their values are accounted for in the general ledger as debits and credits. A company can maintain one journal for all transactions, or keep several journals based on similar activity (e.g., sales, cash receipts, revenue, etc.), making transactions easier to summarize and reference later. For every debit journal entry recorded, there must be an equivalent credit journal entry to maintain a balanced accounting equation.

Ledgers

A ledger is a record of accounts. The ledger is a permanent summary of all amounts entered in supporting Journals which list individual transactions by date. These accounts are recorded separately, showing their beginning/ending balance.

A journal lists financial transactions in chronological order, without showing their balance but showing how much is going to be charged in each account. A ledger takes each financial transaction from the journal and records it into the corresponding account for every transaction listed. The ledger also sums up the total of every account, which is transferred into the balance sheet and the income statement. There are three different kinds of ledgers that deal with book-keeping:

- Sales ledger, which deals mostly with the accounts receivable account. This ledger consists of the records of the financial transactions made by customers to the business.

- Purchase ledger is the record of the purchasing transactions a company does; it goes hand in hand with the Accounts Payable account.

Tag:Book keeping, CAfoundation, CAfoundationaAccounts, CAfoundationClasses, CAfoundationEconomic, CAfoundationFees, CAfoundationLaw, CAfoundationRegistration, commerce, commerceachiever, CommerceAndAccountancy, CommerceBaba, day books, double entries, Journals, ledger, Objectives of accounting, pettycash book, single entries

You may also like