Contra Account-Meaning,Example,Recording Contra Account (Commerce Achiever)

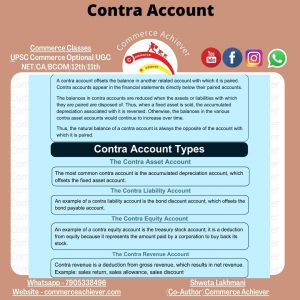

A contra account is used in a general ledger to reduce the value of a related account when the two are netted together. A contra account’s natural balance is the opposite of the associated account. If a debit is the natural balance recorded in the related account, the contra account records a credit.

Understanding Contra Accounts

Contra accounts are reported on the same financial statement as the associated account. For example, a contra account to accounts receivable is a contra asset account. This type of account could be called the allowance for doubtful accounts or bad debt reserve. The balance in the allowance for doubtful accounts represents the dollar amount of the current accounts receivable balance that is expected to be uncollectible. The amount is reported on the balance sheet in the asset section immediately below accounts receivable. The net of these two figures is typically reported on a third line.

KEY POINTS

- A contra account is an account used in a general ledger to reduce the value of a related account.

- They are useful to preserve the historical value in a main account while presenting a decrease or write-down in a separate contra account that nets to the current book value.

- Contra accounts are presented on the same financial statement as the associated account, typically appearing directly below it with a third line for the net amount.

Accountants use contra accounts rather than reduce the value of the original account directly to keep financial accounting records clean. If a contra account is not used, it can be difficult to determine historical costs, which can make tax preparation more difficult and time-consuming. By keeping the original dollar amount intact in the original account and reducing the figure in a separate account, the financial information is more transparent for financial reporting purposes.

Contra accounts provide more detail to accounting figures and improve transparency in financial reporting.

Recording Contra Accounts

When a contra asset account is first recorded in a journal entry, the offset is to an expense. For example, an increase in the form of a credit to allowance for doubtful accounts is also recorded as a debit to increase bad debt expense.

When accounting for assets, the difference between the asset’s account balance and the contra account balance is referred to as the book value. There are two major methods of determining what should be booked into a contra account. The allowance method of accounting allows a company to estimate what amount is reasonable to book into the contra account. The percentage of sales method assumes that the company cannot collect payment for a fixed percentage of goods or services that it has sold. Both methods result in an adjustment to book value.

Examples of Contra Accounts

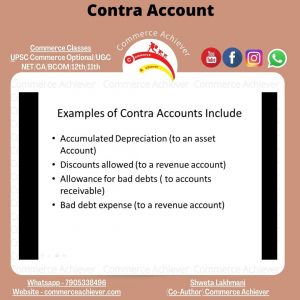

Another example of a contra asset account is the accumulated depreciation account which reduces the reporting value of capital assets. Allowance for obsolete inventory or obsolete inventory reserve are also examples of contra asset accounts. Sales returns is a contra revenue account as the figure is a negative amount net against total sales revenue. It would appear on the company’s income statement in the revenue section.

You may also like