Carrying amount(Carrying Value)-Meaning,Calculation formula,Depreciation in the Carrying Amount (Commerce Achiever)

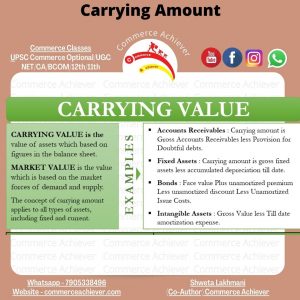

Carrying value is an accounting measure of value in which the value of an asset or company is based on the figures in the respective company’s balance sheet. For physical assets, such as machinery or computer hardware, carrying cost is calculated as (original cost – accumulated depreciation). If a company purchases a patent or some other intellectual property item, then the formula for carrying value is (original cost – amortization expense).

KEY POINTS

- Carrying value is a measure of value for a company’s assets.

- Carrying value is typically measured as the original cost of the asset, minus any depreciating factors. The depreciating factors for an asset vary based on the nature of the asset.

- Some assets, such as land, are not considered depreciable.

- Rates of depreciation for an asset are influenced by the calculations of the company by which it is owned.

How Carrying Value Works

Carrying amount, also known as carrying value, is the cost of an asset less accumulated depreciation. The carrying amount is usually not included on the balance sheet, as it must be calculated. However, the carrying amount is generally always lower than the current market value.

Accounting practice states that original cost is used to record assets on the balance sheet, rather than market value, because the original cost can be traced to a purchase document, such as a receipt. Market value is more subjective. At the initial acquisition of an asset, the carrying value of that asset is the original cost of its purchase. However, over time, the value of an asset will change.

How to Calculate for Carrying Amount

It is a very simple task to calculate for carrying amount, as shown in the example above. But to make it clearer, let’s explain it below:

- Take the original cost of purchasing the asset less salvage value.

- Divide that number by the number of years the asset is expected to be of use to generate the annual depreciation amount and record annually.

- Calculate the accumulated depreciation (number of years past * annual depreciation)

- Subtract the accumulated depreciation from the original purchase price to get the carrying amount.

Depreciation in the Carrying Amount

Depreciation is the lowering of the value of a tangible asset because of wear and tear. Tangible assets include buildings, equipment, furniture, and vehicles. One of the easiest and most commonly accepted methods of computing for depreciation is the straight line depreciation method. Using the straight-line method, the same depreciation value is copied for every year, such as what was done in the above example wherein if the depreciation value for the first year , it would be the same value for the succeeding years.

The other method is the double-decline balance depreciation method otherwise known as the 200% declining balance method. With the DDB method, the depreciation is faster than that of straight-line but will not make the depreciation value bigger. It just means that depreciation is bigger in the early years but smaller in the later years.

You may also like