Accrual-Meaning,Example (Commerce Achiever)

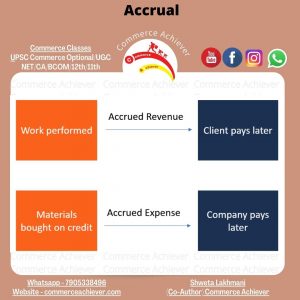

Accruals are revenues earned or expenses incurred which impact a company’s net income on the income statement, although cash related to the transaction has not yet changed hands. Accruals also affect the balance sheet, as they involve non-cash assets and liabilities. Accrual accounts include, among many others, accounts payable, accounts recieveable, accrued tax liabilities, and accrued interest earned or payable.

KEY POINT

- Accruals are needed for any revenue earned or expense incurred, for which cash has not yet been exchanged.

- Accruals improve the quality of information on financial statements by adding useful information about short-term credit extended to customers and upcoming liabilities owed to lenders.

- Accruals and deferrals are the basis of the accrual method of accounting.

- Accruals are created via adjusting journal entries at the end of each accounting period.

Understanding Accruals

Accruals and deferrals are the basis of the accrual method of accounting, the preferred method by Generally accepted accounting principles (GAAP).1 Using the accrual method, an accountant makes adjustments for revenue that has been earned but is not yet recorded in the general ledger and expenses that have been incurred but are also not yet recorded. The accruals are made via adjusting general entries at the end of each accounting period, so the reported financial statements can be inclusive of these amounts.

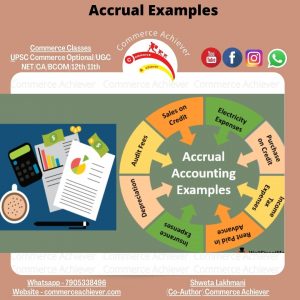

Examples of Accruals

Let’s look at an example of a revenue accrual for an electric utility company. The utility company generated electricity that customers received in December. However, the utility company does not bill the electric customers until the following month when the meters have been read. To have the proper revenue figure for the year on the utility’s financial statements, the company needs to complete an adjusting journal entry to report the revenue that was earned in December.

It will additionally be reflected in the receivables account as of December 31, because the utility company has fulfilled its obligations to its customers in earning the revenue at that point. The adjusting journal entry for December would include a debit to accounts receivable and a credit to a revenue account. The following month, when the cash is received, the company would record a credit to decrease accounts receivable and a debit to increase cash.

An example of an expense accrual involves employee bonuses that were earned in 2019, but will not be paid until 2020. The 2019 financial statements need to reflect the bonus expense earned by employees in 2019 as well as the bonus liability the company plans to pay out. Therefore, prior to issuing the 2019 financial statements, an adjusting journal entry records this accrual with a debit to an expense account and a credit to a liability account. Once the payment has been made in the new year, the liability account will be decreased through a debit, and the cash account will be reduced through a credit.

Another expense accrual occurs for interest. For example, a company with a bond will accrue interest expense on its monthly financial statements, although interest on bonds is typically paid semi-annually. The interest expense recorded in an adjusting journal entry will be the amount that has accrued as of the financial statement date. A corresponding interest liability will be recorded on the balance sheet.

You may also like