Current Assets-Meaning,Key Components of Current Assets,Formula,Financial Ratios Using Current Assets or Their Components (Commerce Achiever)

Current assets represent all the assets of a company that are expected to be conveniently sold, consumed, used, or exhausted through standard business operations with one year. Current assets appear on a company’s balance sheet, one of the required financial statements that must be completed each year.

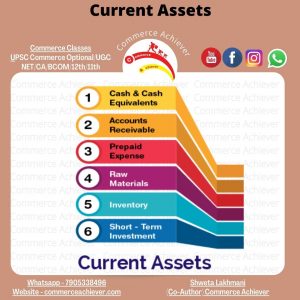

Current assets would include cash, cash equivalents,accounts recieveables, stock inventory, marketable securities, pre-paid liabilities, and other liquid assets. Current assets may also be called current accounts.

KEY POINTS:

- Current assets are all the assets of a company that are expected to be sold or used as a result of standard business operations over the next year.

- Current assets include cash, cash equivalents, accounts receivable, stock inventory, marketable securities, pre-paid liabilities, and other liquid assets.

- Current assets are important to businesses because they can be used to fund day-to-day business operations and to pay for the ongoing operating expenses.

Understanding Current Assets

Current assets contrast with long-term assets, which represent the assets that cannot be feasibly turned into cash in the space of a year. They generally include land, facilities, equipment, copyrights, and other illiquid investments.

Current assets are important to businesses because they can be used to fund day-to-day business operations and to pay for ongoingoperating expenses. Since the term is reported as a dollar value of all the assets and resources that can be easily converted to cash in a short period, it also represents a company’s liquid assets.

However, care should be taken to include only the qualifying assets that are capable of being liquidated at the fair price over the next one-year period. For instance, there is a strong likelihood that many commonly used Fast moving consumer goods (FMCG) goods produced by a company can be easily sold over the next year. Inventory is included in the current assets, but it may be difficult to sell land or heavy machinery, so these are excluded from the current assets.

Depending on the nature of the business and the products it markets, current assets can range from barrels of crude oil, fabricated goods, work in progress inventory, raw materials, or foreign currency.

Key Components of Current Assets

Cash, cash equivalents, and liquid investments in marketable securities, such as interest-bearing short-term Treasury bills or bonds, are obvious inclusions in current assets. However, the following are also included in current assets:

Accounts Receivable

Accounts receivable—which is the money due to a company for goods or services delivered or used but not yet paid for by customers—are considered current assets as long as they can be expected to be paid within a year. If a business is making sales by offering longer terms of credit to its customers, a portion of its accounts receivables may not qualify for inclusion in current assets.

It is also possible that some accounts may never be paid in full. This consideration is reflected in an allowance for doubtful accounts, which is subtracted from accounts receivable. If an account is never collected, it is written down as a bad debt expenses, and such entries are not considered current assets.

Inventory

Inventory—which represents raw materials, components, and finished products—is included as current assets, but the consideration for this item may need some careful thought. Different accounting methods can be used to inflate inventory, and, at times, it may not be as liquid as other current assets depending on the product and the industry sector.

For example, there is little or no guarantee that a dozen units of high-cost heavy earth-moving equipment may be sold over the next year, but there is a relatively higher chance of a successful sale of a thousand umbrellas in the coming rainy season. Inventory may not be as liquid as accounts receivable, and it blocks working capital. If the demand shifts unexpectedly, which is more common in some industries than others, inventory can become backlogged.

Prepaid Expenses

Prepaid Expenses—which represent advance payments made by a company for goods and services to be received in the future—are considered current assets. Although they cannot be converted into cash, they are the payments already made. Such components free up the capital for other uses. Prepaid expenses could include payments to insurance companies or contractors.

On the balance sheet, current assets are normally displayed in order of liquidity; that is, the items that are most likely to be converted into cash are ranked higher. The typical order in which current assets appear is cash (including currency, checking accounts, and petty cash), short-term investments (such as liquid marketable securities), accounts receivable, inventory, supplies, and pre-paid expenses.

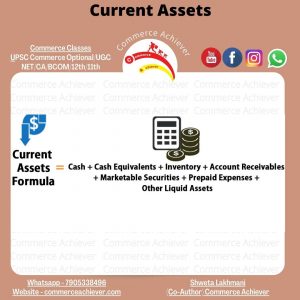

The Formula For Current Assets

Thus, the current assets formulation is a simple summation of all the assets that can be converted to cash within one year. For instance, looking at a firm’s balance sheet, we can add up:

Uses of Current Assets

The total current assets figure is of prime importance to the company management with regards to the daily operations of a business. As payments toward bills and loans become due at the end of each month, management must be ready to spend the necessary cash. The dollar value represented by the total current assets figure reflects the company’s cash and liquidity position and allows management to prepare for the necessary arrangements to continue business operations.

Additionally, creditors and investors keep a close eye on the current assets of a business to assess the value and risk involved in its operations. Many use a variety of liquidity ratios, which represent a class of financial metrics used to determine a debtor’s ability to pay off current debt obligations without raising external capital. Such commonly used ratios include current assets (or parts thereof) as a component of their calculations.

Financial Ratios Using Current Assets or Their Components

Due to different attributes attached to business operations, different accounting methods, and different payment cycles, it can be challenging to correctly categorize components as current assets over a given time horizon. The following ratios are commonly used to measure a company’s liquidity position. Each ratio uses a different number of current asset components against the current liabilities of a company.

- The current ratio measures a company’s ability to pay short-term and long-term obligations and takes into account the total current assets (both liquid and illiquid) of a company relative to the current liabilities.

- The quick ratio measures a company’s ability to meet its short-term obligations with its most liquid assets. It considers cash and equivalents, marketable securities, and accounts receivable (but not the inventory) against the current liabilities.

- The cash ratio measures the ability of a company to pay off all of its short-term liabilities immediately and is calculated by dividing the cash and cash equivalents by current liabilities.

While the cash ratio is the most conservative ratio as it takes only cash and cash equivalents into consideration, the current ratio is the most accommodating and includes a wide variety of components for consideration as current assets. These various measures are used to assess the company’s ability to pay outstanding debts and cover liabilities and expenses without having to sell fixed assets.

Tag:CAfoundation, CAfoundationaAccounts, CAfoundationClasses, CAfoundationEconomic, CAfoundationFees, CAfoundationLaw, CAfoundationRegistration, commerce, commerceachiever, CommerceAndAccountancy, CommerceBaba, Current assets, Financial Ratios Using Current Assets or Their Components, Key Components of Current Assets

You may also like