Current liabilities-Meaning,Eample,calculation,Features,Accounting for Current Liabilities (Commerce Achiever)

Current liabilities are a company’s short-term financial obligations that are due within one year or within a normal operating cycle. An operating cycle, also referred to as the cash conversion cycle, is the time it takes a company to purchase inventory and convert it to cash from sales. An example of a current liability is money owed to suppliers in the form of account payable.

An example of a current liability is money owed to suppliers in the form of account payable.

Understanding Current Liabilities

Current liabilities are typically settled using current assets, which are assets that are used up within one year. Current assets include cash or accounts receivables, which is money owed by customers for sales. The ratio of current assets to current liabilities is an important one in determining a company’s ongoing ability to pay its debts as they are due.

Accounts payable is typically one of the largest current liability accounts on a company’s financial statements, and it represents unpaid supplier invoices. Companies try to match payment dates so that their accounts receivables are collected before the accounts payables are due to suppliers.

For example, a company might have 60-day terms for money owed to their supplier, which results in requiring their customers to pay within a 30-day term. Current liabilities can also be settled by creating a new current liability, such as a new short-term debt obligation.

KEY POINTS

- Current liabilities are a company’s short-term financial obligations that are due within one year or within a normal operating cycle.

- Current liabilities are typically settled using current assets, which are assets that are used up within one year.

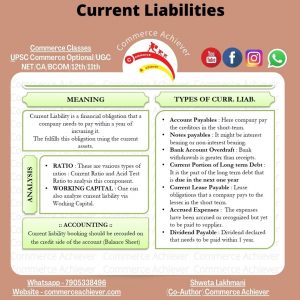

- Examples of current liabilities include accounts payable, short-term debt, dividends, and notes payable as well as income taxes owed.

Examples of Current Liabilities

Below is a list of the most common current liabilities that are found on the balance sheet:

- Accounts payable

- short-term debt such as bank loans or commercial paper issued to fund operations

- Dividends payable

- Notes payable—the principal portion of outstanding debt

- Current portion of deffered revenue, such as prepayments by customers for work not completed or earned yet

- current maturities of long term debt

- Interest payable on outstanding debts, including long-term obligations

- Income taxes owed within the next year

Sometimes, companies use an account called “other current liabilities” as a catch-all line item on their balance sheets to include all other liabilities due within a year that are not classified elsewhere. Current liability accounts can vary by industry or according to various government regulations.

How Current Liabilities are Used

Analysts and creditors often use the current ratio. The current ratio measures a company’s ability to pay its short-term financial debts or obligations. The ratio, which is calculated by dividing current assets by current liabilities, shows how well a company manages its balance sheet to pay off its short-term debts and payables. It shows investors and analysts whether a company has enough current assets on its balance sheet to satisfy or pay off its current debt and other payables.

The quick ratio is the same formula as the current ratio, except it subtracts the value of total inventories beforehand. The quick ratio is a more conservative measure for liquidity since it only includes the current assets that can quickly be converted to cash to pay off current liabilities.

A number higher than one is ideal for both the current and quick ratios since it demonstrates there are more current assets to pay current short-term debts. However, if the number is too high, it could mean the company is not leveraging its assets as well as it otherwise could be.

The analysis of current liabilities is important to investors and creditors. Banks, for example, want to know before extending credit whether a company is collecting—or getting paid—for its accounts receivables in a timely manner. On the other hand, on-time payment of the company’s payables is important as well. Both the current and quick ratios help with the analysis of a company’s financial solvency and management of its current liabilities.

Accounting for Current Liabilities

When a company determines it received an economic benefit that must be paid within a year, it must immediately record a credit entry for a current liability. Depending on the nature of the received benefit, the company’s accountants classify it as either an asset or expense, which will receive the debit entry.

You may also like