Fundamental Accounting Assumptions-Going concern, Consistency, Accural (Commerce Achiever)

Fundamental Accounting Assumptions

Accounting assumptions are the three very basic accounting concepts or principles that are assumed to have been followed in the accounting transactions of an entity. So there is a need for a specific notation saying such concepts have been adhered to, it is understood.

However, this does not mean that such fundamental accounting principles have to be compulsorily followed by all organizations. It is absolutely acceptable if the entity does not follow such assumptions while recording their financial transactions. If these fundamental assumptions have not been followed then the entity should specifically disclose this information, along with their financial statements. This way the users know about such facts.

Now let us take a look at the three accounting assumptions as per the Accounting Standards of India.

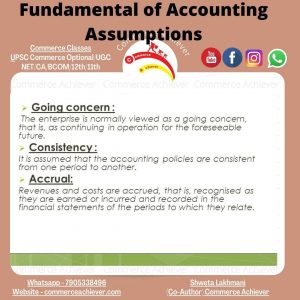

1] Going Concern

This assumption is based on the principle that while making the financial statements of an entity we will assume that the company has no plans of winding up in the near future. So the assumption is that the company will continue to exist indefinitely (far into the future), i.e. it will keep on going.

This assumption is important as it allows for the appropriate accounting of fixed assets and depreciation. Since traditionally we follow the historical cost method for valuation of assets, we have to assume that the business is in no danger of being shut down in the future. If this is the case then such assets will have to be valued at market value. But in the case of a going concern, we do not take into account the increase/decrease in prices of assets.

Another case would be that of expenses written off over a number of years like Deferred Advertising Expense. The benefit of such an expense is enjoyed over a number of years. So instead of charging the expense in one year, we amortize it. This is also possible due to the going concern assumption.

2] Consistency

This assumption states that unless and until things are mentioned in the accounting policies, procedures, standards, etc, Things that have been followed in accounting remains the same. This allows for uniformity in the financial statements of a company over the years. It also becomes easier to compare financial statements from the previous years, something that is important to potential investors and other external stakeholders.

When the accounting treatments and methodologies remain the same over a period of several years the management can properly draw conclusions about the performance of a company. It is an important aspect of planning and decision-making functions of management.

However, this does not mean that an entity cannot change accounting policies to stay relevant with times. This assumption does not completely prohibit change. Sometimes it is necessary to make changes under the following conditions

- If it is a statutory requirement and the entity will have to change its accounting policy to abide by the law

- Other times a change in policy will allow them to represent their accounts more fairly and appropriately.

- Changes made so books of accounts can be in compliance with the Accounting Standards issued by the ICAI

So when the entity changes their policies or methods for the above reason, the users of the financial statements must be informed. Whether there is a material effect in the current year or upcoming years a disclosure must be made. This disclosure is usually made in the notes at the end of the balance sheet.

3] Accrual

Under this assumption, accounting transactions are recorded in the books of accounts when they occur. This is known as the Mercantile System. So as opposed to the cash system, in accrual concept, the revenue or expenditure is recognized in the year they are realized.

According to this concept, the revenue will be recognized in the year it has been realized in. So say firm XYZ and Co. made credit sales in January of 2020 of 10,000/-. And by 31st March they had received only 7,000/- with 3,000/- still receivable. However, the entire 10,000/- will be recognized in the year 2019-2020, irrespective of how much money was actually received.

Similarly in case of expenses also it is irrespective whether actual cash was paid or not. Expenses are to be recognized in the year in which they facilitate the earnings of revenue. So if the annual electricity bill of XYZ Co. of Rs 20,000/- is unpaid by 1st April, it will still be in the books as Outstanding Expense.

You may also like