Section 6(1) – Exception of Residential Status of Individual

Income Tax Provisions

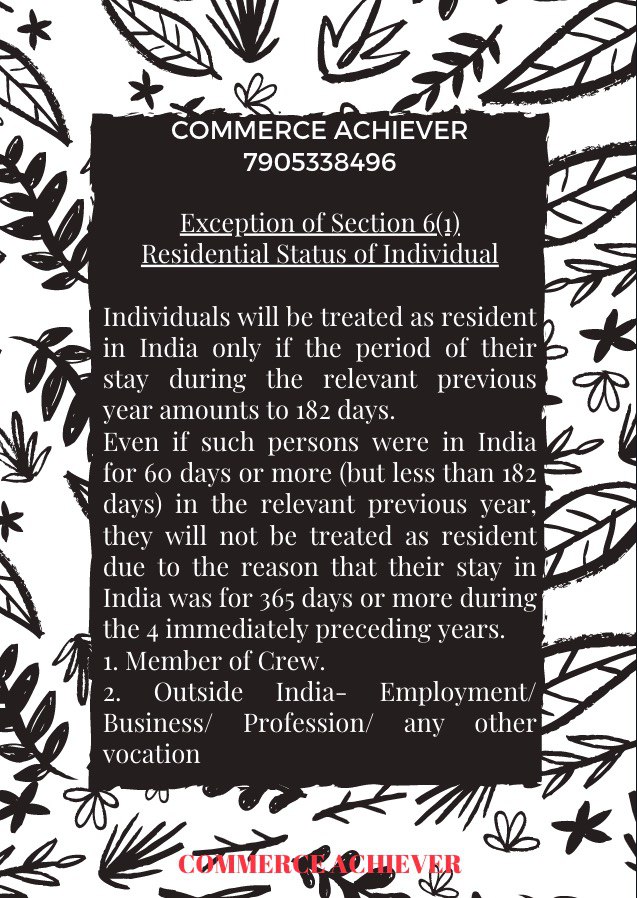

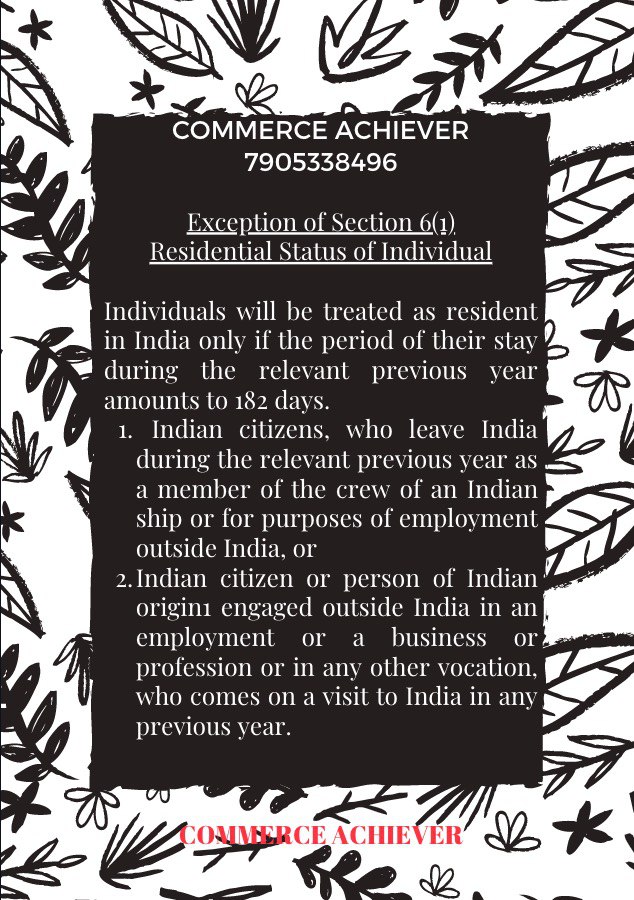

Exceptions to General Conditions [Sec 6(1)]

The following categories of individuals will be treated as resident in India only if the period of their stay during the relevant previous year amounts to 182 days or more.

ie. For the following persons, the condition in (a) of Basic condition shall apply to determine their Residential Status-

- An individual is an Indian Citizen, leaving India for employment outside India during the relevant previous year.

- Indian citizen being a Crew Member of an Indian Ship, leaving India during the relevant previous year.

- Individual being Indian Citizen or Person of Indian Origin engaged outside India in an employment or a Business or Profession or in any other vocation and visiting India during the relevant previous year. (A person is said to be of Indian origin if he or either of his parents or either of his grandparents were born in undivided India).

Note-

- If the above person stays in India for less than 182days, they will be considered as Non-Resident.

- Leaving India for Employment outside India also includes Self-Employment outside India.

- Determination of Residential of Crew Member of a Ship: Individual being an Indian Citizen and Member of the Crew of a Foreign bound Ship leaving India, the period(s) of stay in India shall, in respect of such voyage shall be determined in the manner and subject to such prescribed conditions. For determining the period of Stay in India, the following period shall NOT include-

Period beginning from – Date entered into the Continuous Discharge Certificate in respect of joining the ship by the said Individual for the eligible voyage.

Period Ending to – Date entered into continuous discharge certificate in respect of the signing off by that individual from the ship in respect of such voyage.

- Eligible Voyage – shall mean a voyage undertaken by a ship engaged in the carriage of passengers or freight in international traffic where-

- For the voyage having originated from any port in India, has its destination as any port outside India and

- For the voyage originated from any port outside India, has its destination as any port in India.

- Continuous Discharge Certificate – This term has the meaning assigned to it in the Merchant Shipping (Continuous Discharge Certificate-cum Seafarer’s Identity Document) Rules, 2001 made under the Merchant Shipping Act, 1958.

For Numerical – Refer to Youtube What 5 Years of Bodybuilding Taught Me About Tackling Mondays abs workout bodybuilding coach eugene teo breaks down top calves exercises Channel.

For Complete Course or Book (Videos on provisions, Numericals, Tests, Guidance, etc) –

CONTACT US-

Tag:commerce, commerce achiever, commerce optional, Exception of Residential Status of Individual, Residential Status for crew member, Residential Status for Individual, Residential Status for Individual as Crew Member, Residential Status for individual employment outside india, Residential Status for Individual under Income Tax, Residential status for the purpose of income tax, Residential status in india, Residential Status under Income Tax, Section 6(1) Residential Status, upsc commerce optional, upsc commerce optional paper, upsc commerce optional previous year paper, upsc commerce optional syllabus, upsc optional

You may also like

")