Balance Sheet-Meaning,Share holder’s equity,Assets,liabilities,limitations of balance sheet (Commerce Achiever)

A balance sheet is a financial statement that reports a company’s assets, liabilities and shareholders’ equity at a specific point in time, and provides a basis for computing rates of return and evaluating its capital structure. It is a financial statement that provides a snapshot of what a company owns and owes, as well as the amount invested by shareholders.

The balance sheet is used alongside other important financial statements such as the income statement and statement of cash flows in conducting fundamental analysis or calculating financial ratios.

KEY POINTS

- A balance sheet is a financial statement that reports a company’s assets, liabilities and shareholders’ equity.

- The balance sheet is one of the three (income statement and statement of cash flows being the other two) core financial statements used to evaluate a business.

- The balance sheet is a snapshot, representing the state of a company’s finances (what it owns and owes) as of the date of publication.

- Fundamental analysts use balance sheets, in conjunction with other financial statements, to calculate financial ratios.

Formula Used for a Balance Sheet

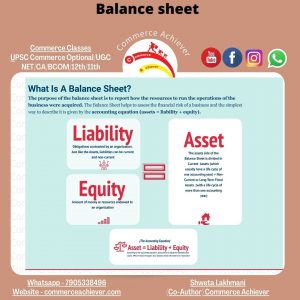

The balance sheet adheres to the following accounting equation, where assets on one side, and liabilities plus shareholders’ equity on the other, balance out:

You may also like

What are the functions of Cost Accounting?

June 16, 2023