• The expression ‘control and management’ referred to under section 6 refers to the central control and management and not to the carrying on of day-to-day business by servants, employees or agents. • The business may be done from outside …

• The expression ‘control and management’ referred to under section 6 refers to the central control and management and not to the carrying on of day-to-day business by servants, employees or agents. • The business may be done from outside …

Resident: A HUF would be resident in India if the control and management of its affairs is situated wholly or partly in India. Non-resident: If the control and management of the affairs is situated wholly outside India it would become …

Individuals can be resident but not ordinarily resident in India. A not-ordinarily resident person is one who satisfies any one of the conditions specified under section 6(6). (i) If such individual has been non-resident in India in any 9 out …

(a) The term “stay in India” includes stay in the territorial waters of India (i.e. 12 nautical miles into the sea from the Indian coastline). Even the stay in a ship or boat moored in the territorial waters of India …

Individuals will be treated as residents only if the period of their stay during the relevant previous year amounts to 182 days. In other words even if such persons were in India for 365 days during the 4 preceding years …

Under section 6(1), an individual is said to be resident in India in any previous year, if he satisfies any one of the following conditions: (i) He has been in India during the previous year for a total period of …

The incidence of tax on any assessee depends upon his residential status under the Act. For all purposes of income-tax, taxpayers are classified into three broad categories on the basis of their residential status viz. (1) Resident and ordinarily resident …

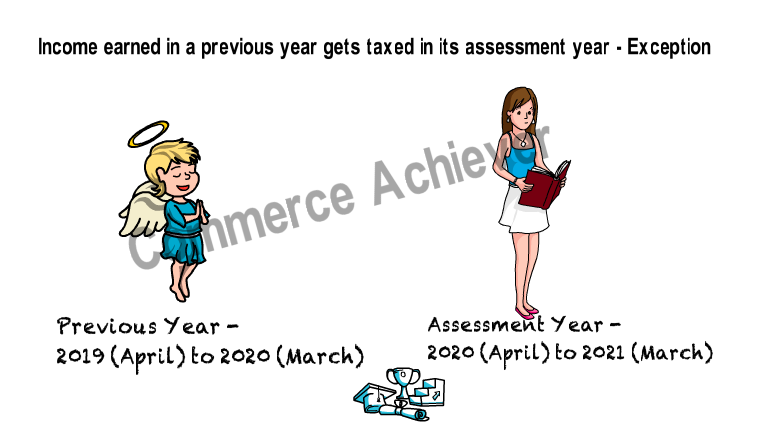

Normally, income earned in a previous year gets taxed in its assessment year. However, in certain cases, where income is not disclosed by the taxpayer but is detected by the Income Tax department and the source for which is not …

Normally, income earned in a previous year gets taxed in its assessment year. However, in certain cases, where income is not disclosed by the taxpayer but is detected by the Income Tax department and the source for which is not …

Assessment year The term has been defined under section 2(9). This means a period of 12 months commencing on 1st April every year. The year in which income is earned in the previous year and such income is taxable in …