Residential status of Individuals-Important Points

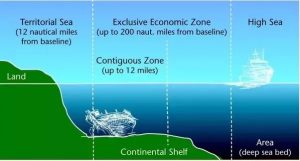

(a) The term “stay in India” includes stay in the territorial waters of India (i.e. 12 nautical miles into the sea from the Indian coastline). Even the stay in a ship or boat moored in the territorial waters of India would be sufficient to make the individual resident in India.

(b) It is not necessary that the period of stay must be continuous or active nor is it essential that the stay should be at the usual place of residence, business or employment of the individual.

(c) For the purpose of counting the number of days stayed in India, both the date of departure as well as the date of arrival are considered to be in India.

(d) The residence of an individual for income-tax purpose has nothing to do with citizenship, place of birth or domicile. An individual can, therefore, be resident in more countries than one even though he can have only one domicile.

Tag:11 commerce, 11th commerce, 12 commerce, 12th commerce, ASSESSMENT YEAR, Barnard-Simon Theory, Barnard-Simon Theory of Organizational Equilibrium, bba, bcom, ca, ca cpt, ca final, ca inter, commerce, commerce achiever, commerce optional, cs, cs final, cs inter, direct tax, Income earned in a previous year gets taxed in its assessment year - Exception, income tax, mba, mcom, Organization Equilibrium, PREVIOUS YEAR, PREVIOUS YEAR AND ASSESSMENT YEAR, Residential Status, Residential status of Individuals, Residential status of Individuals Important Points, tax, Theory of Organizational Equilibrium, ugc net, ugc net commerce, ugc net commerce optional, upsc commerce optional, upsc commerce optional paper, upsc commerce optional previous year paper, upsc commerce optional syllabus, upsc optional